Ready to Refi? Your Mortgage Refinancing Checklist is Here

Ready to trade your current mortgage for a better one? You’ve heard the buzz: refinancing can lower your monthly payments, reduce your interest rate, or even help you consolidate high-interest debt. It’s one of the smartest moves you can make as a financial planning strategy for homeowners. But let’s be real: thinking about gathering all that paperwork? That’s where most of us get stuck. And that’s why we’re providing you with the ultimate refinancing checklist to ensure your application is submitted quickly and approved without a hitch. This post is your comprehensive, zero-fluff guide. By the end, you’ll know precisely how to prepare for your mortgage refinance journey.

Phase 1: Identity Documents on the Refinancing Checklist

The first step in any refinance application and our ultimate refinancing checklist is confirming that you are, well, you. Lenders need to verify your identity and ensure the property is your primary residence (if that’s the type of loan you’re applying for). Having these foundational documents ready is the best way to kick off your process quickly.

Essential Identity Documents

- Government-Issued Photo ID: A valid driver’s license or passport for all borrowers.

- Social Security Card: Your lender will need the numbers for all applicants to run a credit check and verify income.

- Proof of Residency: Typically, this is confirmed by the address on your ID. However, some lenders may ask for a recent utility bill to verify your current residence.

Phase 2: Income and Employment Verification

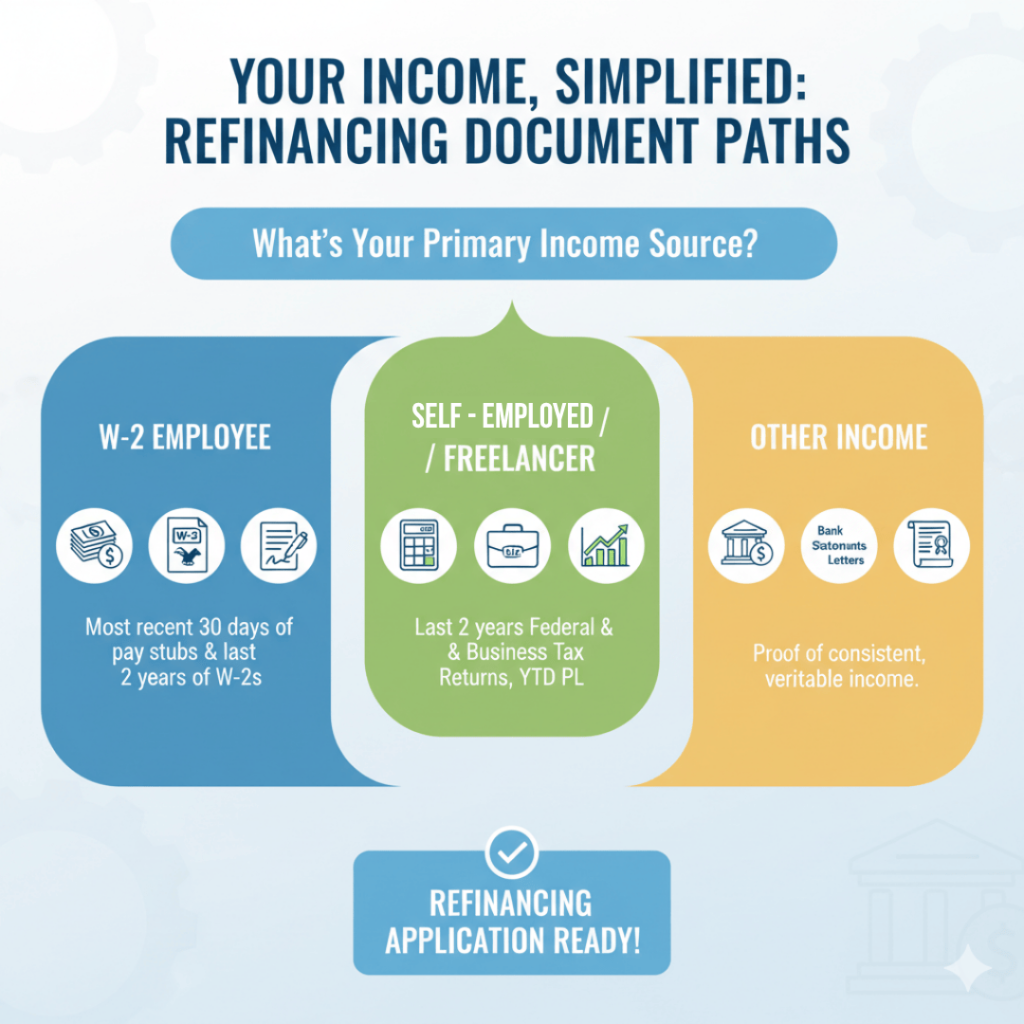

This is often the most scrutinized section of your application. Lenders want a crystal-clear picture of your financial stability to ensure you can comfortably handle the new mortgage payments. If you’re self-employed, an independent contractor, or have multiple income streams—which is common for our target audience—it’s vital to have these details organized. This information is crucial for those asking: What documents do I need for a mortgage refinance?

The Income Checklist for W-2 Employees

- Pay Stubs: Your most recent 30 days’ worth of consecutive pay stubs.

- W-2 Forms: Copies of your W-2 forms for the last two full calendar years.

- Proof of Additional Income: If you receive a bonus, commission, or have a second job, you’ll need documentation (like an employment letter) to prove its frequency and stability.

Gathering Tax Documents for Self-Employed Homeowners to Refinance

If you are your own boss, your tax returns are your primary proof of income.

- Federal Tax Returns: Complete copies of your signed federal tax returns (Form 1040) for the past two years, including all schedules (especially Schedule C or Schedule K-1).

- Business Tax Returns: If your business is structured as a corporation or partnership, you’ll need the past two years of business tax returns.

- Year-to-Date Profit & Loss Statement: This helps the lender see your current financial standing.

Phase 3: Assets and Debts on the Refinancing Checklist

The lender needs to confirm you have the funds for closing costs and to understand your overall debt-to-income (DTI) ratio. A lower DTI ratio is a key component of financial planning for younger homeowners and getting favorable refi terms.

Bank Statements and Investments

- Bank Statements: The most recent two months of statements for all checking and savings accounts. Lenders will be looking for large, non-payroll deposits, which may require a written explanation.

- Investment/Retirement Accounts: The most recent two months of statements for any brokerage, 401(k), IRA, or other investment accounts. You may need these to prove you have reserves after closing.

Current Debt Documentation

- Current Mortgage Statement: Your most recent statement showing the loan number, current principal balance, and monthly payment. For context on long-term savings, you might find our article on the different loan terms helpful: 30-Year Fixed vs. 15-Year Fixed.

- Other Debt Statements: Recent statements for auto loans, credit cards, student loans, or personal loans. You don’t need to gather everything—a full credit report will capture most of this—but statements can help clarify recent payments or balances.

Phase 4: Property and Insurance Details

Your existing property and the associated coverage are the final pieces of the puzzle. The lender is essentially replacing your old loan with a new one, so they need all the documentation related to the asset securing the loan.

Home and Loan Documents

- Current Homeowner’s Insurance Policy: The declarations page showing your coverage, policy number, and the annual premium.

- Property Tax Bill: Your most recent property tax statement to confirm the current tax amount and schedule.

- Current Title Policy (Optional but Helpful): If you still have your original title insurance policy from when you bought the home, it can sometimes help expedite the title process for the refinance. You can find more comprehensive refinancing insights here: InstaMortgage Refinance Hub.

The Refinance Blueprint: Your Next Action Steps

Refinancing doesn’t have to be a headache. By using this Ultimate Refinancing Checklist, you’ve already completed the hardest part: getting organized. The main takeaway for those asking how to streamline the mortgage refinance process is preparation. Having your documents in a single, well-labeled digital folder will shave days or even weeks off your timeline.

The lending industry is moving toward a more streamlined, digital experience, making it easier than ever to submit your paperwork online and track your application’s progress.

Ready to see if a better rate is waiting for you? Take the next step:

Sign up at InstaRefi.com to get free refinance alerts, no credit pull required. This is the easiest way to stay on top of the market and capture the perfect rate opportunity as soon as it appears. For more information about how your personal tax situation affects mortgage eligibility, the IRS has a helpful overview of the different income forms you may need.

You May Also Like:

- 57Do you want to reduce interest cost, pay off your mortgage faster without making a significant difference to current spending or saving habits? If your answer is yes, then the revolutionary new loan, called "All in One" is your answer. The two biggest problems with conventional mortgages are: The majority…

- 57Home Equity Line of Credit (HELOC) is a home mortgage loan that works much like credit cards. It allows you to borrow funds up to a certain established credit limit, usually on as needed basis. However unlike credit cards which are unsecured debts, HELOCs are collateralized against your home. There…

- 54

Understanding rate shopping can save you tens of thousands of dollars. Yes, you read that correctly! That’s why so many home buyers take the extra time to shop around before deciding on a lender to work with. We’ll use this article to help you understand the rate shopping world and…

Understanding rate shopping can save you tens of thousands of dollars. Yes, you read that correctly! That’s why so many home buyers take the extra time to shop around before deciding on a lender to work with. We’ll use this article to help you understand the rate shopping world and…