Understanding a 3-2-1, 2-1, and 1-0 Buydown Mortgage is extremely important in the 2023 housing market with elevated rates and lower affordability.

Understanding 3-2-1 Buydown Mortgage

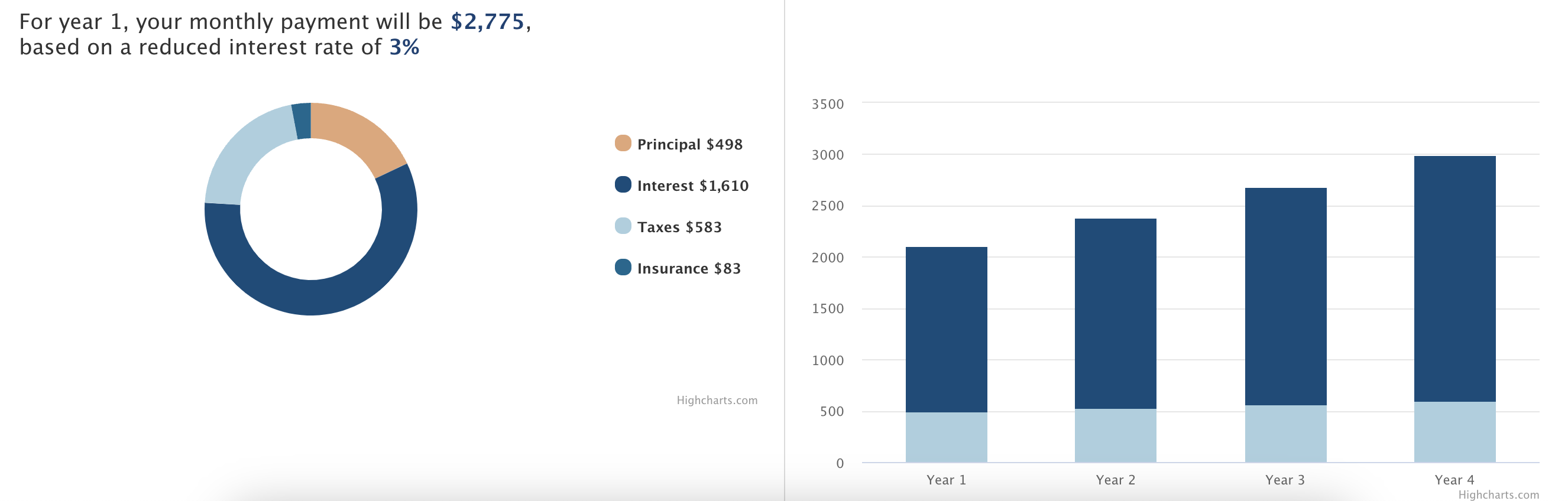

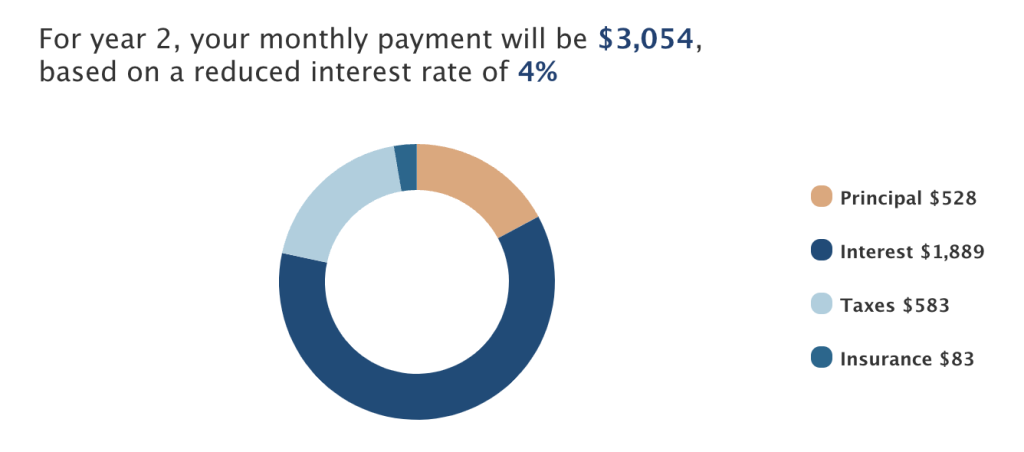

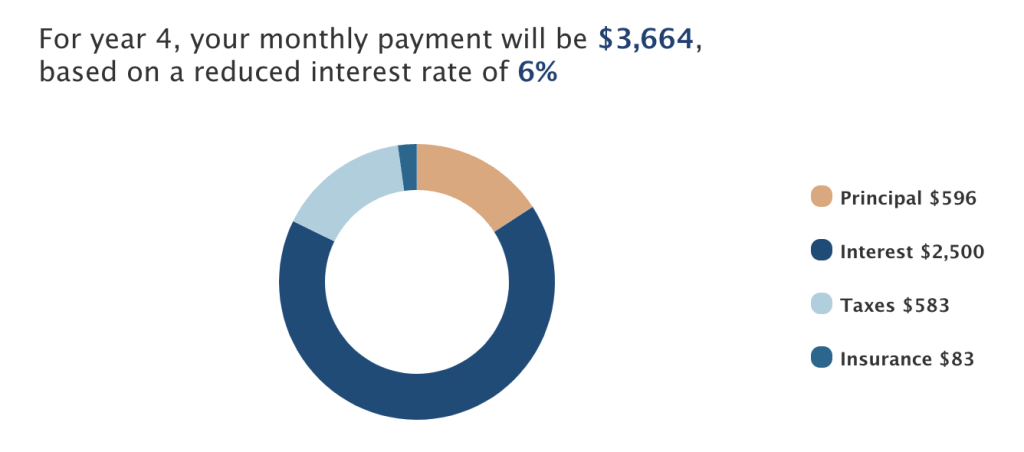

A 3-2-1 buydown mortgage starts at 3% lower than your note rate in year 1, 2% lower in year 2, and 1% lower in year 3. So, if you get a rate of 6%, your first-year monthly payment will be calculated at 3%, second year at 4%, third year at 3%, and then goes back to your note rate (i.e. 6%) for the rest of the term of the loan.

Let’s look at an example – Say your loan amount is $500,000 at a note rate of 6%. Let’s also assume that the yearly property tax is $7,000 and the homeowner’s insurance is $1000/year. For the 1st year, your monthly payment will be at 3%. See the chart below for the breakdown.

Run your customized calculation using our buydown mortgage calculator

Understanding 2-1 Buydown Mortgage

A 2-1 buydown mortgage starts at 2% lower than your note rate in year 1, and 1% lower in year 2. So, if you get a rate of 6%, your first-year monthly payment will be calculated at 4%, your second year at 5%, and then goes back to your note rate (i.e. 6%) for the rest of the term of the loan.

Let’s look at an example – Say your loan amount is $500,000 at a note rate of 6%. Let’s also assume that the yearly property tax is $7,000 and the homeowner’s insurance is $1000/year. For the 1st year, your monthly payment will be at 4%. See the chart below for the breakdown.

Run your customized calculation using our buydown mortgage calculator

Understanding 1-0 Buydown Mortgage

A 1-0 buydown mortgage starts at 1% lower than your note rate in year 1. So, if you get a rate of 6%, your first-year monthly payment will be calculated at 5%, and then goes back to your note rate (i.e. 6%) for the rest of the term of the loan.

Let’s look at an example – Say your loan amount is $500,000 at a note rate of 6%. Let’s also assume that the yearly property tax is $7,000 and the homeowner’s insurance is $1000/year. For the 1st year, your monthly payment will be at 3%. See the chart below for the breakdown.

Run your customized calculation using our buydown mortgage calculator

Who Pays for the Difference Between the Expected Payment and the Actual Payment

In the 3-2-1 example, the total buydown is $21,769, for the 2-0 example, the total; buydown is $11,092 and in the 1-0 buydown mortgage example, the total buydown fee is $3,764.

This is the upfront one-time fee that you need to pay to qualify for these loan programs. You should work with your agent to see if you can get the buydown fees paid by the seller. That way you can get up to a 3% lower rate in year one without paying any extra closing costs from your pocket.

Why should I choose to go with a Buydown Mortgage?

A buydown mortgage allows you to make a lower monthly payment in the initial year(s). Once the rate goes down, you can refinance into a lower rate anyway. But while the market rates are elevated, you could still make your monthly payments at a lower rate. So, it’s a short-term play while we are waiting for the rates to go down.

With the real estate markets slightly softer than in the last few years, sellers might be more willing to pay you for these discount points as an incentive to get their properties sold. Given the expectations that the rates might go down later this year or early next year, you could consider a 1-0 buydown mortgage thus reducing your upfront cost.

You May Also Like:

- 61

For the last 30+ years, lenders have been using Fico scores. More mortgage lenders have the option to use Vantage credit scores starting in Q1 or 2024. You should understand the difference between Vantage and Fico credit scoring and what impacts them. What Scoring Model will Mortgage Lenders be using?…

For the last 30+ years, lenders have been using Fico scores. More mortgage lenders have the option to use Vantage credit scores starting in Q1 or 2024. You should understand the difference between Vantage and Fico credit scoring and what impacts them. What Scoring Model will Mortgage Lenders be using?… - 58

Whether you are a first-time home buyer, looking to buy a second home or an investment property, the first step is to understand the mortgage pre approval process so that you can get a pre approval letter. What is a pre-approval? The mortgage pre-approval process is where a lender reviews…

Whether you are a first-time home buyer, looking to buy a second home or an investment property, the first step is to understand the mortgage pre approval process so that you can get a pre approval letter. What is a pre-approval? The mortgage pre-approval process is where a lender reviews… - 56

Your credit score and credit history are vital to the mortgage process. In this guide, we break down the basics of credit scores and offer valuable tips on how to manage your score. Start from the beginning or jump in wherever you are to continue! Basics of Credit Scores Introduction…

Your credit score and credit history are vital to the mortgage process. In this guide, we break down the basics of credit scores and offer valuable tips on how to manage your score. Start from the beginning or jump in wherever you are to continue! Basics of Credit Scores Introduction…