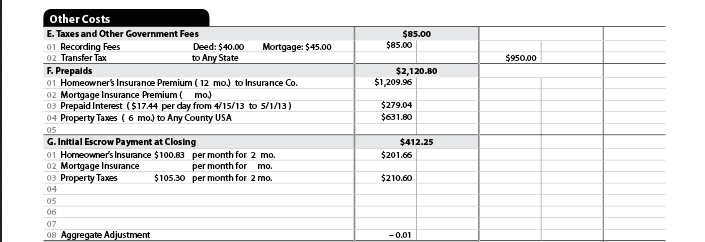

Two of the most confusing sections are Prepaids and Impounds on the Closing Disclosure (CD) – Prepaids (Section F) and Initial Escrow Payment at Closing (Section G). Both these sections are under “Other Costs”.

Understanding Prepaids in Section F on the Closing Disclosure:

01 – Homeowner’s Insurance Premium – You will need to pay 12 months premium at the time of closing if the mortgage is for purchasing a home. If you are refinancing and your insurance is good for more than 60-days at the time of closing, you will not need to pay this.

02 – Mortgage Insurance Premium – Since most mortgage insurance premium is paid monthly along with you regular mortgage payment, this should be $0. However, if you are paying lumpsum for your mortgage insurance – one big upfront payment, you will see that cost added here.

03 – Prepaid Interest – This category includes interest on your loan between the time you close and the end of that month. Note that you would typically skip the monthly payment after that. So, if you are closing the loan on April 15th, you will pay 16 days of interest (see the screenshot above), but will not make a mortgage payment in May. Your first mortgage payment will be due June 1st.

04 – Property Taxes – You would pay for this only if the property taxes are currently due. Note that “due” doesn’t mean the last date by which you can make the payment. For example, in California 1st installment of tax becomes due on October 1st, but can be paid until December 10th without any penalty. However, for any loan closing on or after October 1st, the property taxes have to be paid at closing since there were “due”. If you’re buying a home, you may owe sellers if they have prepaid for taxes beyond the closing date. For example, if you are closing on April 15th, but the sellers have already paid until June 30th, you will need to pay the sellers (reimburse) prorated tax payment from April 15th to June 30th.

Three Different Affordability Calcularors For You to Use

Understanding Initial Escrow (Impounds) Payment in Section G on the Closing Disclosure:

This is where it gets really confusing. Before we get into the calculations of how many months of reserves required for an Escrow (also called impound) account, let’s first understand what is an impound account.

According to Consumer Finacial Protection Bureau–

An escrow account sometimes called an impound account depending on where you live, is set up by your mortgage lender to pay certain property-related expenses. The money that goes into the account comes from a portion of your monthly mortgage payment. An escrow account helps you pay these expenses because you send money through your lender or servicer, every month, instead of having to pay a big bill once or twice a year.

Many lenders require that you pay your taxes and insurance using escrow, so they can make sure that the bill gets paid. Your mortgage servicer will manage the escrow account and pay these bills on your behalf. Sometimes, escrow accounts may also be required by law.

Let’s break it down. Let’s take the example of Texas where taxes are due annually.

Mortgage Pre-Approval

in Minutes

Here is the formula for Property Taxes:

A+B-C

A = Total # of Months in the Year (This is always 12)

B = Total # of Months of Reserves (This is always 2 and mandated by federal mortgage guidelines, meaning lenders always need to have 2 extra months of reserves than they need. So if they have to pay 12 months of taxes, they need to have 14 months on that date. This protects the lender in case of any missed payment by the borrower)

C = Total # of Months Between 1st Mortgage Payment and Next Tax Instalment due date

Again, if you close a loan on April 15th in Texas and the next installment of Property Tax is due on December 1st, then you would have made 7 months of the mortgage payment before December 1st (June – November).

Using the formula above = 12 (A)+2 (B) – 6 (C) = 8 months of property taxes to be collected at closing.

So you would pay 7 months upfront + 7 monthly payments so that the lender will have the required 14 months of payment on December 1st. The lender would pay 12 months of tax payment to the county and 2 months of additional reserves will stay in your escrow account and will show on your escrow balance on your mortgage statement.

The formula for Homeowner’s Insurance is exactly the same:

A = Total # of Months in the Year (This is always 12)

B = Total # of Months of Reserves (This is always 2)

C = Total # of Months Between 1st Mortgage Payment and Next Insurance renewal date

Again, if you close a refinance loan on April 15th in Texas and the next insurance renewal date is January 1st, then you would have made 8 months of the mortgage payment before December 1st (June – December).

Using the formula above = 12 (A)+2 (B) – 7 (C) = 7 months of Homeowner’s Insurance to be collected at closing.

So you would pay 6 months upfront + 8 monthly payments so that the lender will have the required 14 months of payment on January 1st. The lender would pay 12 months of insurance premium to your homeowner’s insurance company and 2 months of additional reserves will stay in your escrow account and will show on your escrow balance on your mortgage statement.

If you have Flood Insurance:

If your property is in a flood zone, the premium has to be impounded even if your taxes and homeowner’s premium are not. Typically the flood insurance premium is impounded for 2 months.

Hope that helped you understand how the prepaids and impound numbers are calculated for your loan estimate (LE) and closing disclosure (CD).

Finally, if you are looking for general information, this helpful post by Porch contains advice on everything you would need to know about the mortgage process, ranging from underwriting to mortgage insurance, and top tips on finding the best lender for you.

You May Also Like:

- 73

If you have lived in your current home for a few years and thinking of moving up, i.e. buying a bigger and better home, the question that you are most likely thinking is - "Can I buy that home before selling my current home?" Advantages of Selling before Buying: You…

If you have lived in your current home for a few years and thinking of moving up, i.e. buying a bigger and better home, the question that you are most likely thinking is - "Can I buy that home before selling my current home?" Advantages of Selling before Buying: You… - 70

Although every situation is unique, it is not uncommon for homebuyers to qualify for a mortgage on a new home while still living in their primary residence. Perhaps you are outgrowing your current house, or have been forced to relocate due to a job transfer? Regardless of the motivation for…

Although every situation is unique, it is not uncommon for homebuyers to qualify for a mortgage on a new home while still living in their primary residence. Perhaps you are outgrowing your current house, or have been forced to relocate due to a job transfer? Regardless of the motivation for… - 69How to Qualify for a Mortgage with IRS Repayment Plan! Whether you filed your completed taxes this April or an extension, you should already know your tax liability for the past year. If, despite your withholding or quarterly payments, you owe more than you can pay all at once, don’t…