You’re finally ready to become a homeowner, and you want to do everything right in the process. According to your research, realtor, family, and friends – the first step is getting pre-approved by a mortgage lender. The problem is, no one can explain what exactly ‘pre-approved‘ means. A mortgage pre-approval approves you for only one number and that is NOT the purchase price.

A loan pre-approval is not a loan officer doing a quick review of your information and generating a maximum purchase price that you can afford. In reality, a pre-approval is almost as detailed as the full loan approval, and you learn the maximum monthly mortgage payment, known as the PITI, you qualify for, given your income and debts.

Get Pre-Approved for a Mortgage

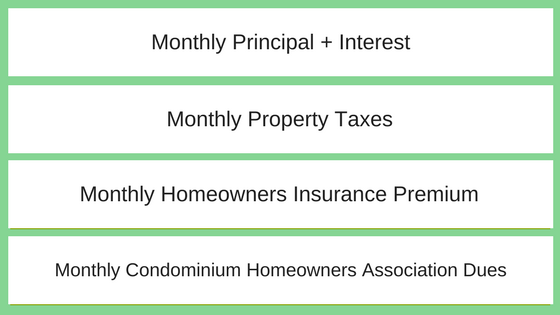

PITI stands for ‘principal, interest, taxes and insurance,’ and those are the ingredients in a monthly mortgage payment. If you’re buying a condominium, the monthly homeowners association (HOA) dues are added to this number (then called the PITIA.)

To determine that maximum monthly payment, the lender will need to review a full credit report, income documentation (pay stubs, W-2’s, and tax returns), and asset statements. The full credit report provides your actual credit score, credit balances and minimum monthly payments for the calculations.

Your income documentation is also critical during a pre-approval, to calculate how much can be used to support the projected monthly debt per underwriting guidelines. All of your income is reviewed, including bonus, commission, or self-employment income (requires your complete federal tax returns.)

Finally, they’ll review the statements for all of your assets – including checking, savings, investment, and retirement accounts – and factor these into the down payment and, if required, the reserves. Once all of your documentation is collected, the debt-to-income calculation process begins.

The analysis is done per one month: monthly income, monthly debts, and monthly PITI. We start with the end in mind – no more than 45% of your gross monthly income can be used to pay the projected monthly debt. For a jumbo mortgage, that drops to 43%. Here’s a breakdown of each component of the calculation:

- Principal & interest payment: calculated by using the approximate loan amount and current interest rate (based on the loan type, credit score, down payment percentage and property type.)

- Property tax: calculated by estimating the purchase price and multiplying that by the approximate annual property tax basis in the specific county. (For example in Santa Clara County, California, property taxes are $1.25 for every $1,000 in value.) The annual amount is broken down into a monthly amount.

- Homeowners insurance: the approximate annual insurance premium for a fire insurance policy is estimated and broken down into monthly payments, like the property taxes.

- HOA Dues: if you are considering buying a condominium or a townhome, the approximate monthly dues are included in the monthly payment.

Added to the above PITI(A) is the total of all the monthly payments on your current outstanding debt, including car loans, student loans, personal loans, and the minimum amounts due on your revolving debt (aka credit card) balances.

Once these are combined, the amount of your projected total monthly debt is divided into your monthly income to determine if it is within the maximum (45%/43%) allowed. While you’re not obligated to purchase a home with a mortgage that would put you at the maximum ratio – you won’t be approved for anything that exceeds that number.

Looking at some real numbers, an $800,000 purchase price with a loan for 80%, or $640,000, gives you the following approximate PITI:

P+I: $3,243 A 30 year fixed rate mortgage @ 4.5% interest

T: $833 Property tax – $1.25/$1,000 in value ($800,000)

I: $150 Homeowners Insurance est. annual premium $1800

Total: $4,226 Full monthly PITI payment

The PITI added to the existing monthly obligations which, for this example, there is $1100 in car payment, student loan, and minimum monthly credit card payments. The combined total monthly debt is $5,326, which is divided by the monthly income previously calculated. We can also divide the total monthly income by .45, which gives the minimum monthly income needed to qualify in this scenario.

After you complete the pre-approval process, keep the ingredients of the calculation in mind as you begin to search for a home. Each of them can decrease, via a lower loan amount, a better insurance premium, or a lower interest rate, however, once you know the maximum payment you qualify for, that’s the ceiling.

Get Pre-approved for a Mortgage

What can increase and, in turn, lower your maximum allowed PITI?

- Rising interest rates

- Higher purchase price

- Higher loan amount

- Higher property taxes

Even a minor increase in the purchase price will impact your debt-to-income ratio as it means higher property taxes and possibly a higher loan amount. Making a more substantial down payment will keep the principal and interest payment stable, but won’t lower the property tax amount. And don’t forget the last piece of the equation — a change in your income will also impact the debt-to-income ratio.

While you can’t control interest rates, property tax rates or insurance premiums, some of the numbers are within your control. You can save for a more substantial down payment or pay down your monthly debt to increase your maximum qualifying PITI.

So, there you have it. You are not actually pre-approved for a maximum purchase price, but a certain PITI payment.

You May Also Like:

- 10000

Steps to Take After Mortgage Pre-Approval! If you’re a homebuyer that’s made it to the pre-approval stage, pat yourself on the back. You've crossed a significant milestone on your journey to homeownership. But what happens after you've been pre-approved for a mortgage? Here are the steps you need to take…

Steps to Take After Mortgage Pre-Approval! If you’re a homebuyer that’s made it to the pre-approval stage, pat yourself on the back. You've crossed a significant milestone on your journey to homeownership. But what happens after you've been pre-approved for a mortgage? Here are the steps you need to take… - 10000

Whether you are a first-time home buyer, looking to buy a second home or an investment property, the first step is to understand the mortgage pre approval process so that you can get a pre approval letter. What is a pre-approval? The mortgage pre-approval process is where a lender reviews…

Whether you are a first-time home buyer, looking to buy a second home or an investment property, the first step is to understand the mortgage pre approval process so that you can get a pre approval letter. What is a pre-approval? The mortgage pre-approval process is where a lender reviews… - 10000

Getting a mortgage qualification letter prior to looking for a new home with an agent is an essential first step in the home buying process. Besides providing the home buyer with an idea of their monthly payments, down payment requirements and loan program terms, a Pre-Approval Letter gives the seller…

Getting a mortgage qualification letter prior to looking for a new home with an agent is an essential first step in the home buying process. Besides providing the home buyer with an idea of their monthly payments, down payment requirements and loan program terms, a Pre-Approval Letter gives the seller…