The Million-Dollar Question: Will Refinance Rates Drop in the Near Future?

If you bought a home between 2023 and 2024, you’ve probably spent the last year thinking the same thing: “When are these rates going to drop so I can refinance?” You’re not alone. Many new homeowners, especially tech-savvy ones who value financial optimization, are eagerly watching economic indicators for a shift. The dream of snagging a sub-6% mortgage, which seemed impossible just months ago, is slowly becoming a potential reality.

The good news? The market trend is downward. The bad news? It won’t be a straight line.

Mortgage and refinance rate drop possibilities are tied to the Federal Reserve’s battle against inflation, economic growth, and the volatile 10-year Treasury yield. While many experts project rates to continue their slow and modest decline through the end of 2025 and into 2026, the specific timing and depth of the drops remain a puzzle. In this post, we’ll dive into the current forecasts, break down the key factors influencing your refinance opportunity, and show you exactly how to prepare for the moment the market moves in your favor.

🔮 Expert Forecasts: Where Are Refinance Rates Headed?

Current economic data—particularly softening inflation and a cooling jobs market—suggest the Federal Reserve’s (the Fed) monetary policy is working. Historically, a weakened labor market and lower inflation often lead to a lower federal funds rate, which tends to pull mortgage rates down as well.

Here’s what major financial authorities are predicting for the average 30-year fixed mortgage rate:

| Forecasting Authority | End of 2025 Forecast | End of 2026 Forecast |

| Mortgage Bankers Association (MBA) | ≈ 6.5% | ≈ 6.4% |

| Fannie Mae | ≈ 6.4% | ≈ 5.9% |

| J.P. Morgan Research | Potential decline of up to 60 basis points over the next year | Cautiously optimistic for further declines |

Key Takeaway: The consensus leans toward rates stabilizing in the mid-6% range through late 2025, with a much clearer possibility of rates dipping below 6% in 2026 (Source: Fannie Mae, Mortgage Bankers Association).

If your current mortgage rate is above the mid-6% range, this downward trajectory means you need to be ready to act fast to capitalize on a future refinance rate drop.

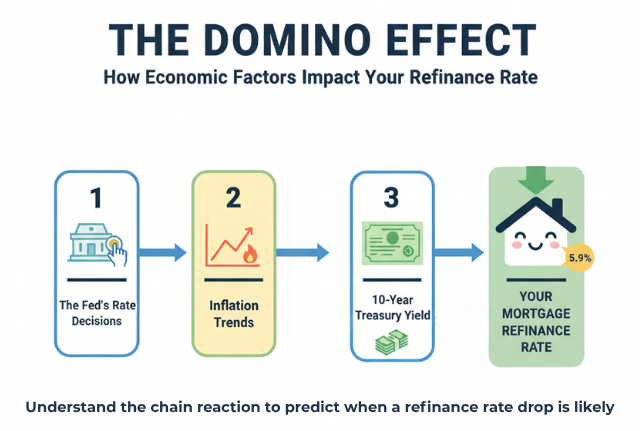

What Drives a Refinance Rate Drop?

Refinance rates move in response to several economic and market conditions, including inflation, Federal Reserve policy, and housing demand. Understanding these variables gives you insight into when a refinance rate drop might occur.

-

Inflation trends: When inflation slows, long‑term borrowing costs—like mortgage rates—tend to decline.

-

Federal Reserve decisions: The Fed’s rate cuts or pauses can directly influence mortgage rates, though not immediately.

-

Economic growth: Slower economic expansion usually leads to lower rate environments as investors shift toward safer assets like U.S. Treasury bonds.

According to recent industry reports from Freddie Mac and Mortgage Bankers Association (external authoritative sources), analysts expect moderate mortgage‑rate easing into early 2026—especially if inflation remains stable and unemployment edges up slightly.

Pro Tip: Before rates decline further, gather your financial documents so you’re ready to act fast. Use The Ultimate Refinancing Checklist: Documents You’ll Need on InstaMortgage.com to stay organized.

🚀How to Prepare for the Next Rate Drop

The biggest mistake homeowners make is waiting for the perfect rate, often missing a great opportunity because they’re not prepared. Here’s your refinancing strategy for next rate cut guide.

I. Optimize Your Personal Financial Profile

Even a significant refinance rate drop won’t matter if your personal finances aren’t in shape. Lenders offer the best rates to the lowest-risk borrowers.

- Boost Your Credit Score: A score of 740 or higher is often the minimum threshold to qualify for the most competitive rates. Pay down revolving debt, dispute any errors on your credit report, and keep credit utilization low.

- Lower Your Debt-to-Income (DTI) Ratio: Lenders want to see your total monthly debt payments (including the new mortgage payment) are low compared to your gross monthly income. Lowering your DTI ratio shows greater financial stability.

- Build Your Home Equity: A Loan-to-Value (LTV) ratio of 80% or lower is ideal, as it may allow you to eliminate Private Mortgage Insurance (PMI) and qualify for better terms. Learn more about how refinancing can help you eliminate PMI and save money here.

II. Choose the Right Refinancing Path

When you pull the trigger on a refinance, you have two main options:

- Rate-and-Term Refinance: The most common type. This simply changes your interest rate and/or the length of your loan term to lower your monthly payment and save on interest.

- Cash-Out Refinance: This replaces your old mortgage with a new, larger one, allowing you to take the difference in cash. This is a popular way to fund major renovations or consolidate high-interest debt, an essential part of financial planning for younger homeowners.

III. The Tactical Approach: Don’t Wait for the Bottom

Waiting for the absolute lowest rate is a gamble. If rates drop significantly, a flood of refinance applications will follow, potentially causing lenders to raise their rates back up due to capacity constraints and overwhelming demand (Source: Kiplinger). The current refinance rates are already substantially lower than the 2023 high of 8%.

✅ Is Now a Good Time to Refinance? Key Decision Factors

Instead of fixating on the national average, focus on your individual “break-even point.”

| Decision Factor | Checkpoint | Your Next Step |

| Refinance Savings | Is the new rate at least 0.25% lower than your current rate? | Yes? Proceed to calculate savings. |

| Closing Costs | Can you recoup the closing costs (typically 1-3% of the loan amount) within 3-5 years? | Calculate your break-even point now. |

| Long-Term Plan | Do you plan to own the home for longer than the break-even period? | If not, refinancing may not be worth the cost. |

| PMI Elimination | Will refinancing help you get rid of Private Mortgage Insurance? | This is often a huge monthly saving—a major reason to refinance! |

Don’t Miss the Next Refinance Rate Drop: The Bottom Line 🎯

While expert forecasts suggest the biggest Refinance Rate Drop is likely to occur over the next two years, the trend is heading in the right direction. For new homeowners, preparation is the key to seizing the opportunity. By optimizing your credit, improving your DTI, and understanding the market factors, you position yourself to save thousands in interest over the life of your loan. Don’t let market volatility cost you the chance to lower your payments.

Ready to stop guessing and start planning?

Sign up at InstaRefi.com to get free refinance alerts, no credit pull required. Be the first to know when a lower rate opportunity hits your personal savings threshold!

You May Also Like:

- 78

Since there are many reasons a homeowner may choose to refinance, we'll take a look at the four most common. 1. Mortgage Rates Drop: Typically, the most common reason that homeowners refinance their mortgage is to secure a lower interest rate. Interest rate and loan amount determines the total cost…

Since there are many reasons a homeowner may choose to refinance, we'll take a look at the four most common. 1. Mortgage Rates Drop: Typically, the most common reason that homeowners refinance their mortgage is to secure a lower interest rate. Interest rate and loan amount determines the total cost… - 78Why the Right Refinance Calculator is Your Ultimate Financial Hack Your mortgage is likely your biggest monthly expense, but what if you could cut that payment by hundreds of dollars—or save tens of thousands over the life of your loan? With interest rates constantly fluctuating and home equity building over…

- 72Shopping for the best Mortgage rate possible has always been the primary objective when borrowing a home loan. As well it should be! The challenge with this strategy is that there is much misleading information released on the subject by various media. Internet websites and email marketing, along with other…